We spoke to Jeremy Tan, who’s running for elections in Mountbatten SMC, about his novel promise of implementing Bitcoin policies.

“That’s the core idea of Bitcoin: erosion-proof money.” said Jeremy Tan, the Bitcoin candidate, as we conversed online about making Bitcoin accessible to all.

Entering as an independent candidate in the Mountbatten Single Member Constituency (SMC) for the coming 2025 Singaporean general elections, Jeremy stands out amongst the different political parties with a bold new topic: Bitcoin.

Taking his campaign to the neighbourhood of Mountbatten, he espouses the need to integrate the digital asset into the nation’s economic framework to safeguard wealth, hedge against inflation, and future-proof the Singapore Dollar.

But Bitcoin and cryptocurrencies aren’t strangers to the world of politics. Earlier this year, US President Trump signed an Executive Order to establish a Strategic Bitcoin Reserve, while countries like Brazil and the Czech Republic are considering establishing reserves of their own.

More recently, fears of a potential recession resulting from the tariff wars initiated by the United States have left businesses in Singapore worrying about rising costs, with nearly half of those surveyed planning to pass on increased costs to their customers.

While the local conversation around cryptocurrencies is often one of speculation and risk, analysts have pointed out that Bitcoin maintains a close correlation to the movement of gold prices, an asset that is seen as a safe haven against risks when markets become volatile.

While Jeremy’s focus on the digital asset seems out-of-place amongst the traditional fiscal policies at first, it’s clear that his campaign centres around the idea of helping Singaporeans beat growing inflation and grow their net worth, albeit with Bitcoin and digital currencies instead of traditional gold and fiat assets.

You’ve made it clear that your focus is on Bitcoin, not other cryptocurrencies. What sets the digital asset apart from the others?

I only focus on Bitcoin because it represents something fundamentally different — it’s an idea rooted in accountability.

Think of it this way: every node on the Bitcoin network is like an accountant, validating and securing the system by using energy — electricity — to maintain the ledger. Bitcoin is essentially a global ledger, protected by a network of machines that run on energy.

In Singapore, we have a situation where 16.5% of people don’t even have S$13,500 to their name. What happens when those savings start to lose value because of the declining reliability of the US dollar?

We need to offer a more secure, inflation-resistant way for them to protect what they have. That’s the responsible thing to do; it’s the ethical thing to do. And it’s something we must work on at a national level.

So, for me, when it comes to long-term savings technology, Bitcoin, powered by Proof-of-Work, is the best use case we have.

Earlier this year, Trump proposed a Strategic Bitcoin Reserve and digital asset stockpile of tokens like XRP, Cardano, and Solana. What are your thoughts on that?

We need to draw a clear line between digital asset reserves and Bitcoin reserves. These are not the same things.

The idea of a strategic Bitcoin reserve still needs to pass through the legislative process. But if you look at what’s happening in places like Wyoming and other Rust Belt states, you’ll notice a trend. These are regions that are facing the threat of industrial decline, and they’re beginning to take Bitcoin more seriously, and with more urgency.

They understand that the trade flows supporting their current livelihoods aren’t guaranteed to last forever; that’s a key point. We’re all vulnerable to disruptions, whether it’s from AI, robotics, or other forces of technological and economic change. And Singapore is no exception.

So, when we talk about reserves, especially Bitcoin reserves, we’re really talking about securing our future. It’s about being forward-looking and asking how we can reduce our vulnerabilities and ensure long-term stability.

What motivated you to make Bitcoin adoption a central pillar of your campaign?

We already believe in inflation and in the importance of protecting ourselves from it. That’s why we allow people to invest their CPF (Central Provident Fund) in the SPDR Gold [Shares] ETF (Exchange-Traded Funds).

If we accept gold as an inflation hedge, then why stop there? The approval of Bitcoin ETFs in late 2023 was a monumental shift in the entire Bitcoin landscape. That change fundamentally re-positioned Bitcoin for every institutional investor — whether mutual funds, retirement schemes, or pension funds — to seriously consider Bitcoin as part of their portfolio. It gave them the framework to conduct their own due diligence.

As a nation, and especially as a politician, I view foreign monetary irresponsibility as a serious concern for Singapore. We do not want to be forced into fiscal policies that erode our autonomy; Bitcoin offers a solution. It’s ethical money, and it allows us to have these difficult national conversations.

You mentioned a surge in volunteer sign-ups for your campaign. Do you see this as a sign of growing public interest in Bitcoin?

I think interest in crypto within Singapore still isn’t in a great place at the moment. The main issue is that the rules, use cases, and potential for Bitcoin at an institutional and business level remain unclear.

People aren’t familiar with how Bitcoin can be integrated into everyday life, and when that clarity is missing, the entire industry suffers. But if we make the framework around Bitcoin clear — the regulations, the use cases, and especially the business incentives — then we’ll start to see real adoption. Once that foundation is in place, everything else will follow naturally.

A study showed that 26% of Singaporeans currently own digital assets. How do you plan to inform the remaining 74% about Bitcoin and its benefits?

Tokens like Solana, GOAT, FTT coin, and others [are assets] I don’t want Singaporeans to get involved with. It’s all speculative, high-risk gambling, and I don’t think we should adopt a speculative mindset. Instead, we should focus on the best savings technologies — those that are inflation-proof and long-term. And within the crypto space, that means Bitcoin.

If Singapore takes Bitcoin seriously, we have a real opportunity to lead. We could create something like a G7-level (A group consisting of seven of the world’s most advanced economies) coordination around Bitcoin policy, regulation, and exchange. This opens the door to better trade flows, consistent regulation, and cross-border insurance frameworks.

Would you say that your message is a familiar strategy in a new packaging, where instead of gold and fiat, it’s now Bitcoin and stablecoins?

Yes. If we look at authors like Saifedean Ammous and Lyn Alden, authors of “The Bitcoin Standard” and “Broken Money”, we begin to understand that humanity has long been in search of a durable, finite ledger. Something that’s divisible, portable, globally recognisable, and trusted as a form of savings — a true currency.

Thanks to modern technology and the emergence of ETFs, Bitcoin has now become that standard. It’s secured by hash rate, protected by decentralised nodes, and continually improved through the Bitcoin Improvement Proposal (BIP) process. The miners safeguard the network by expending energy. This isn’t a quest for high returns, but a pursuit of money that resists erosion.

That’s really the core idea of Bitcoin: erosion-proof money.

I believe Singaporeans stand to benefit greatly from it. But what’s needed is more open discussion, a national conversation about how we can achieve a form of savings that doesn’t get eaten away by inflation. We’ve done it before with CPF and other tools, it’s time to look at Bitcoin in the same light.

Digital assets isn’t a familiar topic to all Singaporeans yet. How do you plan to educate the older or less tech-savvy Singaporeans about Bitcoin?

The best way to explain is, it’s wonderful that some of you are already retired or approaching retirement, but we need to think about the next generation. Their incomes are going to be fighting against a tide of US dollar printing, and that affects their ability to build a secure future.

So the question becomes, how do we help them safeguard that future? If the only solution is to continue expanding the supply of paper money, then we’re just going to see prices continue rising. Because all fiat expansion is, at its core, inflation.

Countries like the US and Argentina are exploring national Bitcoin reserves. Where does Singapore stand in your view, and how do you plan to position us in that global shift?

We’re in a unique position because we already have strong USD flows coming into the country. That liquidity gives us the ability to purchase Bitcoin at scale. We also have the infrastructure — DBS, MAS-regulated custodians, and institutional-grade tools — to secure and manage those assets responsibly.

On top of that, my policies would allow pension funds to allocate a portion of their savings into Bitcoin ETFs. Because Singapore is a relatively small and agile nation, we can implement these moves faster than many larger economies.

On a country-to-country basis, I believe Bitcoin adoption in Singapore could outperform our peers in places like Dubai, Hong Kong, Miami, Argentina, the US, and even China.

China currently accounts for around 40% of the global Bitcoin mining activity. That alone suggests they see Bitcoin as a form of strategic insurance, possibly even against the US. It’s clear they’re thinking long-term. And if China isn’t being complacent, and neither is America, then why are we?

Speaking of mining, do you see Singapore ever becoming a Bitcoin mining powerhouse?

We can’t, our energy supply is too limited. It’s very inefficient for us to consider mining at scale. Also, we don’t have significant domestic energy production.

Take Bhutan for instance; they’re powered by hydropower. But for us in Singapore, our advantage isn’t in raw production. Our strength lies in trade flows — actual ships moving through our ports, actual capital moving through our banks and financial systems, and also in tourism.

So, the real question we need to address in Parliament is: how can we harness those unique economic strengths to acquire more Bitcoin, facilitate Bitcoin transactions, and conduct commerce in Bitcoin? That’s the challenge we need to tackle.

If elected, how would you work with MAS in implementing this policy?

Firstly, I would review all the policies that have been previously rejected. That’s our starting point. I’d have honest discussions with them based on where we stand today — what’s changed, what remains the same — and from there, we can assess whether to move forward with specific proposals. That’s our foundation: start with the data, then have the discussion.

We also need our partners to step up, whether it’s in terms of the Digital Payment Token (DPT) framework or other relevant legislation. I believe in group consultations and open industry discussions about Bitcoin because this is a serious national issue. Let’s take a page from the US. They have a ‘Crypto Czar’, they have regulatory bodies like the SEC involved, and the focus is on coordination across the industry.

That’s what we need here too. It’s not a matter of “I say, you do.” It’s more like, “What is everyone saying? Let’s act on that together.” That kind of collaboration is what’s crucial for Singapore.

Bitcoin isn’t immune to market ups and downs; its value fell over 20% in just three months. How would you address public concern about volatility with a Bitcoin Reserve?

There are several instruments Singapore could issue because we’re in a uniquely strong position.

First, Singapore has over S$500 million in official foreign reserves, mostly in gold and US dollars. Second, our trade volume is roughly three times our national GDP. Third, we have long-term CPF savings structures — the Ordinary and Special Accounts (OA and SA) — that we can adapt. These three factors put us in a position to do what other countries cannot.

Market makers, brokers, and options sellers could start building hedging strategies around long-term Bitcoin holdings. In turn, they could offer structured products that allow people to harness Bitcoin’s long-term growth while being hedged in the short term with safer assets like DBS or STI ETFs. That’s one approach.

Another approach is allowing Bitcoin to be held within CPF accounts. This would create opportunities to monetise Bitcoin’s volatility through options strategies. Essentially, we could earn yield by selling volatility, and that income could be channelled into CPF interest payouts for OA and SA accounts.

Third, I’ve suggested a Baby Coin Fund, giving every newborn S$10,000 worth of Bitcoin in a CPF-style savings account. This allows Singaporeans to build wealth from birth and helps to combat wealth inequality.

My own parents weren’t asset holders, and I know that inflation, even at a 2% target, primarily benefits those who already own assets. That’s the goal here, creating upward mobility.

I believe financial institutions will eventually offer a wide range of Bitcoin-linked products. Some will give retail users exposure to Bitcoin’s upside, while the banks manage the long-term risk, often by offsetting it with US dollar-based instruments.

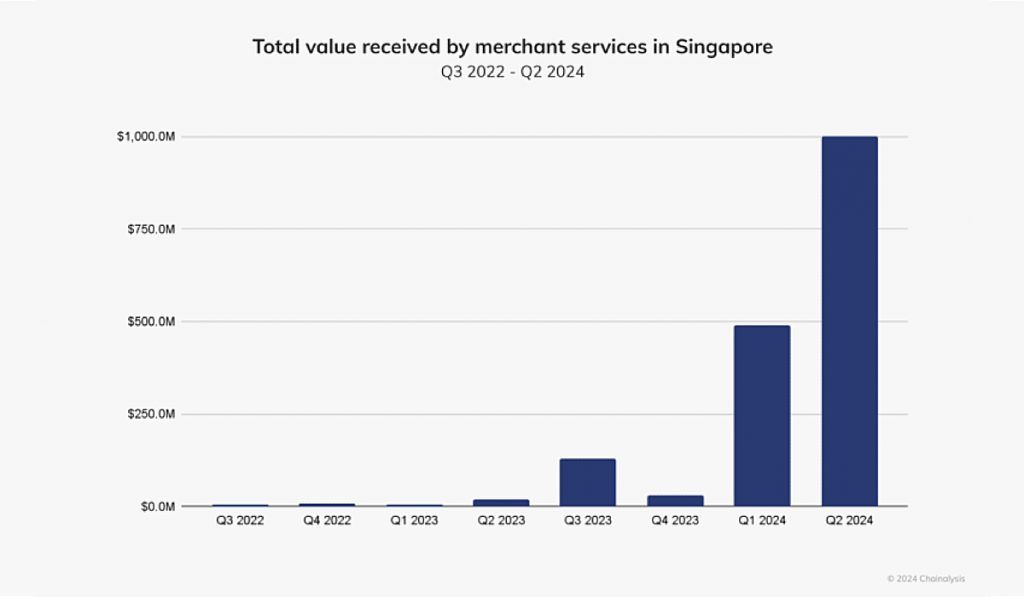

A Chainalysis report showed that crypto payments in Singapore reached nearly $1 billion in Q2 2024. Do you have plans to expand Bitcoin-based payment adoption?

Institutions need to take the first step forward. We’ve already seen earlier attempts at crypto adoption — remember when we had Bitcoin ATMs or small tech startups trying out crypto payment systems? Those efforts didn’t quite take off.

What we need now is for institutions to say, “We can settle certain assets on a Bitcoin standard.” Once that happens, they can then work within their own systems to support broader retail adoption. But realistically, I think we’re still about five to ten years away from seeing people regularly transacting in Satoshis (small units of Bitcoin) on the street.

In the meantime, I believe Bitcoin adoption will begin with its use as collateral. For example, holding Bitcoin could allow someone to access better credit terms, whether it’s for a mortgage, a credit card, or other types of financing. That’s already a familiar model in banking. Fixed deposits and credit are often linked, and I see no reason why Bitcoin couldn’t be included in that framework.

In the short term, I’d focus on integrating Bitcoin into commonly used financial products. That’s the first step — making it easier and more useful for people to hold and leverage Bitcoin within the existing financial system.

With the threat of tariffs and a potential recession on everyone’s mind, how can Bitcoin alleviate fears of economic uncertainty?

We need to start by understanding the real purpose of the tariffs. They’re not designed to reduce American consumption — quite the opposite. They’re meant to create fiscal space so that the US can increase consumption by reducing its debt burden.

The goal is to use tariffs as a negotiation tool, encouraging other countries to absorb some of the US’s debt, thereby lowering the 10-year yield. Consumption is deeply embedded in American culture, from branding and sponsorships to influencer marketing and social media-fuelled spending. It’s not just economic; it’s cultural.

So, where does Bitcoin come in? Bitcoin acts as a form of resistance during trade negotiations. Yes, in the short term, countries may have to accept the terms the US imposes. But holding Bitcoin quietly, as a kind of financial insurance, is a form of long-term protection against fiscal irresponsibility.

Would you then say Bitcoin adoption could strengthen trust in the Singapore dollar, particularly in a recession?

Absolutely, but it’s a nuanced issue. The Singapore dollar (SGD) is already a very well-managed currency. We have a strong AAA rating, and our bonds are consistently oversubscribed, allowing us to offer low yields. Bitcoin adoption could indeed strengthen the SGD, but there’s a flip side.

Investors might start buying up SGD as a proxy for Bitcoin exposure, pushing the currency higher. This speculative demand could be very powerful if harnessed properly. It’s not just about buying and holding SGD — it’s about circulation. If we use Bitcoin to back CPF-linked savings and create Bitcoin-denominated financial products, institutions might start seeing SGD as a kind of beta to Bitcoin, but without the volatility of the US dollar.

That improves our financial credibility, strengthens our currency, and helps shield us from inflation — even though we still settle critical imports like energy and food in USD. It’s a strategic positioning that could redefine Singapore’s role in the global economy.

If elected, would you introduce pro-Bitcoin policies in your constituency?

I would start by introducing programmes focused on education and engagement around how CPF structures can evolve in relation to Bitcoin. But it’s also important to recognise where my residents are coming from.

In my constituency, around 73% of residents live in private property, and social mobility here is the second highest in Singapore. So what they need is support in maintaining the standard of living they’ve worked hard to achieve.

The focus here isn’t radical change, it’s about continuity. They’re looking to preserve stability, and to ensure that their way of life remains sustainable. That’s what matters to them.

Lastly, do you have any parting words for your voters in Mountbatten SMC?

Let’s find out the best way to have inflation-proof assets and inflation-proof pension funds, and we’ll do it together. Mountbatten, let’s do it.