Table Of Contents

If you are scratching your head over this question, you are not the only one. Just as the internet has revolutionised every aspect of our lives, blockchain technology also has the potential to fundamentally change the way things are done. In Singapore, initiatives and associations like the Singapore Blockchain Innovation Programme (SBIP), Blockchain Association Singapore (BAS) and Association of Cryptocurrency Enterprises and Start-ups Singapore (ACCESS) has been launched or formed to champion blockchain implementation. But let’s start from the beginning – What is Blockchain?

What is Blockchain?

Simply put, a blockchain is a database. More specifically, it is a public database that does not store information in a single location and the information stored cannot be corrupted, changed, or easily hacked into. Blockchain is characterised by two main features – its decentralised nature, and the way information is stored in the database. It is able to store information in multiple places at once, thanks to Distributed Ledger Technology (DLT).

Essentially, DLT is a database managed by multiple participants called nodes, and a node can be a computer, server, or storage device. Whenever new information is stored, it is written into a ledger and distributed to every node on the network. This means all information on every node is always updated in real-time, and each node can view the ledger for greater transparency. It also keeps information safe and secure in the event of data failure or a hacking attempt.

How Does This Translate Into Real World Applications?

If you think about public institutions and businesses like hospitals, banks, and telco companies, most of them store critical records such as patient healthcare details, bank information, and your personal data on central servers. Such servers can be targeted by hackers to crack into and steal information easily, and they have happened time and again in the news. With a decentralised system, malicious users would have to gain control of at least 51% of the nodes and reverse the encryption on all nodes to manipulate the system, which makes it much harder to hack. And this brings us to the next point – how does a block of data on a blockchain get locked?

How Does a Block of Data on a Blockchain Get Locked?

Transaction information are stored in groups of data called blocks. Once the block is full, it is then added in a sequence chain to the previous block, hence the name ‘blockchain’. Each block comes with its own timestamp, the details of the transaction records, its own cryptographic hash algorithm, and a reference to the hash algorithm of the previous block. An agreement function by all network nodes called the Consensus Algorithm validates every single block to ensure its accuracy.

Think of the system as a book ledger – every page in the book has a limited amount of space to write transactions in it. When the page is filled up, new information is then written on a new page. Similarly, each block can be considered as a page with its own records but with multiple books being updated at the same time with Distributed Ledger Technology.

Key Features of Blockchain Networks

What makes blockchain technology revolutionary is that it can be applied to multiple industries such as supply chains, banking & finance, and healthcare to make them more efficient, cost-effective, and transparent. This is thanks to the three key features of blockchains below.

Blockchain Networks are Decentralised

Thanks to Distributed Ledger Technology (DLT), information in a blockchain is stored in nodes that make up the network. This also means there is no single person or governing authority who is responsible for the framework which eliminates potential human error.

More importantly, decentralisation makes transactions and information recording faster and cheaper which is of great interest to the payments and finance industry. If you think about the system behind the monetary services, we use daily, there are millions of transactions happening which are supported by a slew of third-party validators and intermediaries.

This makes transactions such as wire transfers and credit card payments expensive for users and businesses alike. Furthermore, banks around the world currently communicate via a global network called SWIFT which communicate messages about financial activities, but the actual execution of transfers goes through a host of intermediaries.

With a decentralised network, block transactions can go from one person to another while skipping the intermediaries in between. Transactions are validated by nodes which removes extra costs, speed up transaction times, and create a secure network by removing intermediaries as potential points of failure.

Blockchain Networks are Secure

Blockchain is considered a secure network due to the way it stores information which boils down to two main functions – hashing and immutable records.

What is hashing? While it sounds like a tasty hash brown, it is a mathematical process that converts information into an encrypted value. Information like transaction details is processed by an algorithm called a hash function, and the string of numbers and letters that comes through is called a hash. The best part? It is impossible to alter and reverse the hashing process as any small change to the hash will lead to a different value altogether. But to ensure that the system is doubly secure, its immutability also comes into play.

Something that is immutable is defined as ‘unchanging over time or unable to be changed’, and that is true for blockchain networks. Once each ‘block’ of info has been hashed, they are added in sequence to the network. Since they are linked in chronological order, each block contains information of the block before it, which has the info of the block before it and so on.

As more and more blocks are added, it becomes harder and harder for malicious users to alter the blockchain as they must make changes to every single block along the chain all the way to the very first block if they want to tamper with the information. At this point, it would be impossible to change the information as the network records are also decentralised and stored in multiple locations, and each of them have a record that refutes any compromised chain. Thus this makes the whole blockchain network immutable and corrupt-proof.

Blockchain Networks use a Consensus Algorithm

Not only does a blockchain network have to be secure, but it also must ensure that all the nodes are maintaining the integrity of the stored information without any of them going out of sync. That’s where the Consensus Algorithm shines – it is essential for maintaining an agreement between all network nodes over the stored information.

To illustrate why there is a need for a consensus algorithm, think back to children’s games such as Pass The Message or the Telephone game. A message is given to the first person, but by the time it reaches the last person the message rarely resembles the initial phrase. While it’s all fun and games in a play setting, it presents a major headache for systems like blockchains where hundreds or thousands of nodes need to store the same information simultaneously and accurately.

Simply put, a consensus algorithm is a computerised way of ensuring all parties of a blockchain network agree on a data in a trustless environment, where participants involved do not need to know or trust each other. This is usually achieved via a majority vote to decide that the data is correct and have it validated as correct within all the stored ledgers. With many nodes validating every transaction and block, a consensus system is critical in making the blockchain run smoothly.

All consensus models ultimately aim to create equality in the system, but each blockchain use different consensus algorithms to achieve faster efficiency. Some well-known examples are the Proof-of-Work (PoW) algorithm first put forth in the 1990s by researcher Markus Jakobsson and implemented by Bitcoin founder Satoshi Nakamoto, the Proof-of-Stake (PoS) consensus that coins like Cardano, Binance coin, and Polkadot utilise, and the Delegated Proof-of-Stake (DPoS) where delegates are selected by stakers to validate transactions in the network.

With consensus, the system can use the least amount of effort to maintain system integrity while ensuring that compromised or bad data is rejected, thus ensuring the system is fault-proof.

Pros and Cons of Blockchain Technology

There are a large number of reasons given by advocates and detractors of Blockchain technology; here’s a summary of the pros and cons.

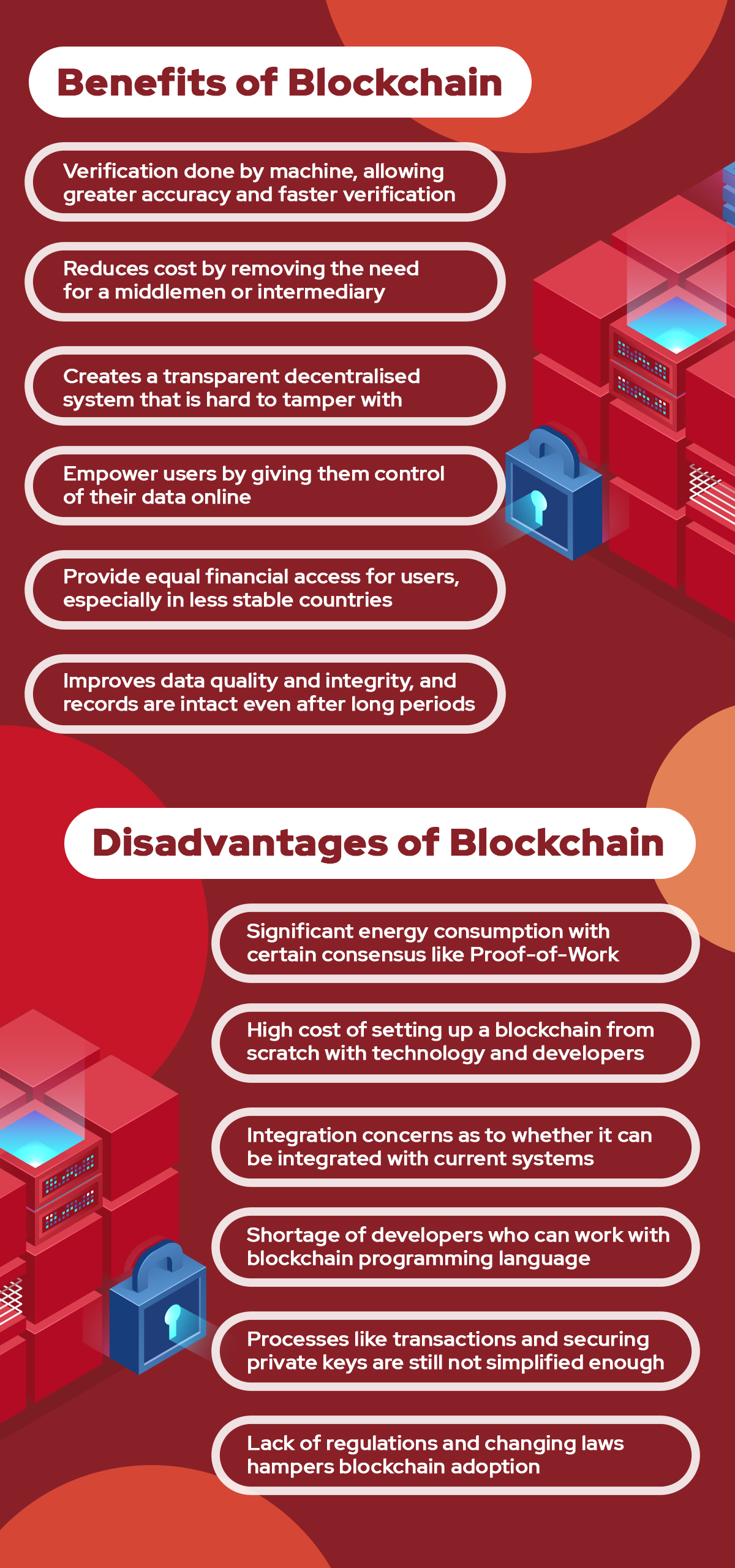

Benefits of Blockchain Technology

Verification Done by Machine: This allows for greater accuracy and faster verification compared to traditional methods, as machines eliminate the risk of human error in the validation process.

Reduces Cost by Removing the Need for a Middleman or Intermediary: Blockchain technology enables direct transactions between parties, which cuts out the need for intermediaries like banks or brokers, thereby reducing transaction fees.

Creates a Transparent Decentralised System that is Hard to Tamper: The decentralised nature of blockchain ensures that no single entity controls the network, enhancing security and making it extremely difficult for anyone to manipulate the data unilaterally.

Empower Users by Giving Them Control of their Data Online: Users have full control over their digital transactions and the sharing of their personal information, enhancing user privacy and autonomy over personal data.

Provide Equal Financial Access for Users, Especially In Less Stable Countries: Blockchain can offer secure, reliable financial services to individuals in countries where traditional banking infrastructures are inadequate or corrupt.

Improves Data Quality and Integrity, and Records are Intact even after Extended Periods: Blockchain’s immutable ledger ensures that once data is entered, it cannot be altered, thus preserving the accuracy and reliability of records indefinitely.

Disadvantages of Blockchain Technology

Significant Energy Consumption With Certain Consensus Like Proof-of-Work: The computational power needed to maintain blockchain networks, especially those that use Proof-of-Work, can lead to excessive energy use, raising environmental concerns.

High Cost of Setting Up a Blockchain From Scratch With Technology and Developers: Developing a blockchain solution involves high initial costs including advanced technology and hiring specialised developers, which can be a barrier to entry for many organisations. Integration Concerns As to Whether It Can Be Integrated With Current Systems: Integrating blockchain technology with existing IT systems can be challenging due to compatibility issues, potentially requiring substantial changes to legacy systems.

Shortage of Developers Who Can Work With Blockchain Programming Language: There is a notable shortage of skilled developers in the blockchain space, which can slow down development and innovation within the industry.

Processes Like Transactions and Securing Private Keys Are Still Not Simplified Enough: The technical complexity of managing blockchain transactions and securing private keys can be a hurdle for average users, limiting its widespread adoption.

Lack of Regulations and Changing Laws Hampers Blockchain Adoption: The rapidly evolving nature of blockchain technology often outpaces the development of relevant regulations, leading to legal uncertainties that can hinder its broader adoption.

Real-life Application of Blockchain Technology

While blockchain is often associated with bitcoin and cryptocurrencies in general, the technology itself has far-reaching effects for various sectors and industries. Some examples are:

Decentralised Applications

While apps are no longer a novel programme thanks to the rapid adoption of smartphones in the last decade, they are still linked to centralised company servers and hosted on app stores of tech giants like Google and Apple with developers following strict guidelines. Decentralised applications (dApps) aim to break away from that by utilising blockchain infrastructure for greater transparency and security, while allowing users to control and own their data. Some popular chains that dApps can be built on are Ethereum, Polkadot, and Solana.

Decentralised Data Storage

With current cloud technologies, storing data on hard drives are a thing of the past. But decentralised data storage projects such as FileCoin and Swarm are taking it to the next level by storing data on multiple nodes maintained by users or groups who are incentivized to join, store, and keep data accessible. Since the information is not stored on a single data server, it is harder for information breaches and outages to occur.

Blockchain Gaming

Earning money from gaming is not a new concept. Whether it’s selling mined gold in World of Warcraft, items in Diablo 3, or selling mesos (or fame) in Maplestory for real money, supply and demand is always present in games. With the introduction of blockchain into gaming, platforms like Enjin and Animoca brands are building games with decentralised features that allow players to earn cryptocurrencies via a ‘Play to Earn’ concept. The cryptocurrency can then be traded on decentralised exchanges, or used to create Non-Fungible Token (NFT) game items which the player can own and store in digital wallets. Axie Infinity and Decentraland are some examples of the current decentralised games in the market.

Real Estate

Real estate is another field that blockchain is in the early process of revolutionising. Companies are slowly recognising the impact the technology has on retail and commercial property sales, while increasing access to real estate investment opportunities. By tokenising real estate property, records of the estate details are recorded clearly and transparent on the blockchain, and they can be easily traded on exchanges and platforms to interested buyers. This eliminates the stigma of property being illiquid assets and removes the long chain of intermediaries in a real estate purchase.

Supply Chains

Imagine being able to track an item from the time it is produced in a factory, all the way to the moment it is sold in a retail store while having accurate details of its journey – that’s what blockchain companies like VeChain are doing to enhance supply chain management and business processes. By integrating blockchain into the process, it streamlines the transaction flows between suppliers, retailers, and banks, while improving product traceability and reducing logistical disruptions.

How are NFTs stored on blockchains?

Non-Fungible Tokens, or NFTs, are unique digital tokens that cannot be replaced, exchanged, copied, or divided into smaller parts. Unlike cryptocurrencies which can be traded 1-for-1, NFTs contain unique information codified by smart contracts on a blockchain which makes each token distinguishable from each other. Think of NFTs as collectibles like rare pokemon cards, signed basketballs, and art paintings.

Similar to the process of storing transaction records, NFT information is also stored as encrypted blocks on the blockchain they are tokenised on; this allows anyone to view the owner of the NFT asset via a block explorer. To tokenise a digital asset into an NFT, creators and artist usually use one of the many NFT platforms such as OpenSea, Mintable, Rarible, Nifty Gateway, or Foundation to mint the NFT and display them for sale.

How are information and assets exchanged on different blockchains?

First off, why are different projects being built on different blockchain projects? Other than choice, each blockchain infrastructure is built with a particular goal in mind which suit the needs of different teams. While Ethereum aims to be the default for blockchain applications, Cardano aims for speed and scalability of up to one million transactions per second, and Cosmos aim to allow developers to create their own chains while allowing them to co-exist and interoperate.

To prevent these projects from becoming isolated ecosystems and allow users on each chain to freely exchange information and assets, Blockchain Interoperability and Cross-Chain Technology are fast becoming a topic of interest for teams to expand. Simply put, chain interoperability and cross-chain technology seek to allow different chains to communicate with one another without the help of intermediary apps or services.

Currently blockchains themselves are building initiatives to bridge the gap, such as the Gravity Bridge in Cosmos’ Gravity Decentralised Exchange, which is a cross-chain bridge to Ethereum DeFi platforms. Other infrastructure chains like Polkadot seek to include cross-chain technology as part of its system by being a multi-chain network that joins other blockchains and sidechains together.

Other notable efforts into creating blockchain interoperability have also been launched by other projects like Near Protocol with its Rainbow cross-chain bridge, and Solana with their Wormhole Bridge which links the network to the Ethereum network.

Looking Ahead: The Expanding Horizon of Blockchain Technology

We revisit the question again – What is Blockchain? We have delved into the different aspects of blockchain in this article, yet the definition is always changing and being re-defined as the technology grows and develops further.

To answer that question in our own words, blockchain is a revolutionary technology that allows us to re-visualise the current status quo of doing things, in a world that is getting more interconnected with a faster, efficient, and more portable internet. With blockchain, the future is only going to get more exciting from hereon.